Formações anteriores

Formação

A ASFAC oferece uma gama de cursos de formação essenciais para quem procura aprofundar conhecimentos e desenvolver competências na área do crédito e educação financeira. Em formato presencial, online ou em e-learning, aceda a conteúdo atualizado e abrangente, contribuindo para o crescimento profissional de excelência.

Formações anteriores

O nosso foco

Formação

Cursos para uma atualização contínua de excelência e para adaptação às mudanças

Literacia Financeira

Iniciativas e conteúdos que pretendem facilitar o acesso de todos à informação

Estatísticas

Compilação dos dados mais relevantes

Legislação

Aceda facilmente à legislação atualizada

Organização

Conheça a equipa profissional que trabalha para os objetivos e missão da ASFAC.

Código de Conduta

Conscientes da importância da harmonização de comportamentos para a defesa dos interesses do mercado de crédito ao consumo em Portugal, tanto para clientes como para entidades financeiras, os associados da ASFAC lançaram, em 2009, o Código de Conduta.

Missão e Valores

Representar os Associados, contribuir para o desenvolvimento do setor e promover a literacia financeira.

A ASFAC é a organização representativa do sector do financiamento especializado ao consumo, contando com 29 membros, dos quais 26 Associados, instituições de crédito especializadas no financiamento ao consumo, que no seu conjunto constituem a quase totalidade do mercado e 3 membros aderentes.

29

membros

26

associados e 3 aderentes

+30

anos

🤝 ASFAC Descomplica 🤝

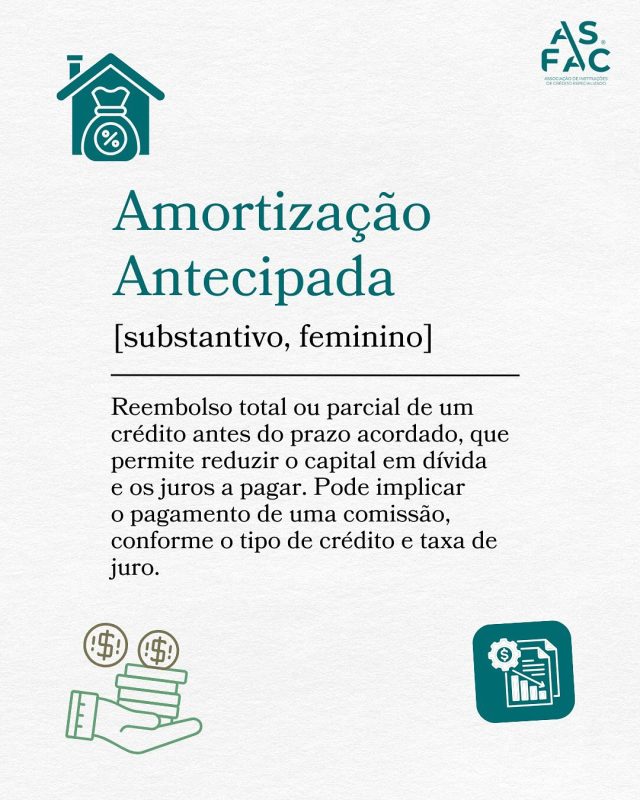

A #amortização antecipada consiste no reembolso total ou parcial de um crédito antes do prazo acordado no contrato. Ao reduzir o...

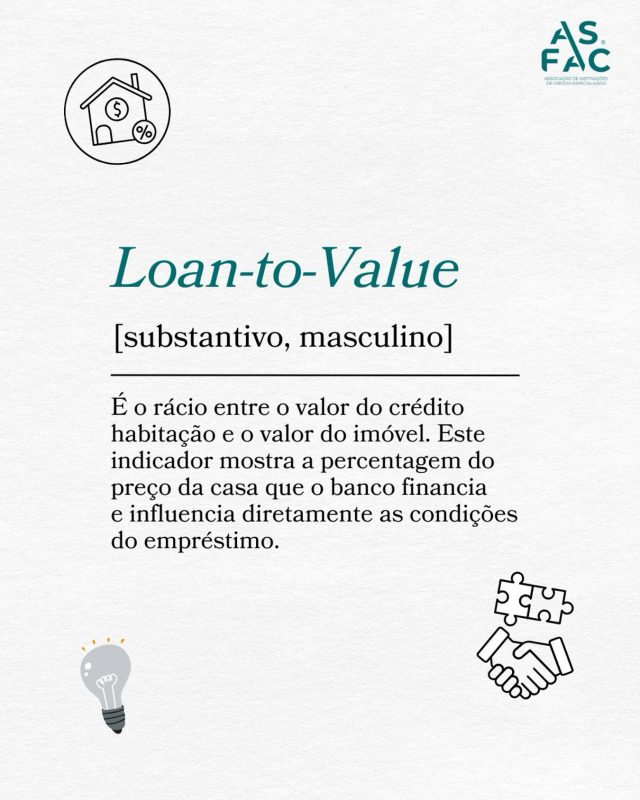

🤔 Sabe o que é o #LTV (Loan-to-Value) e porque é tão importante no momento de pedir um crédito habitação? Este é o conceito que...

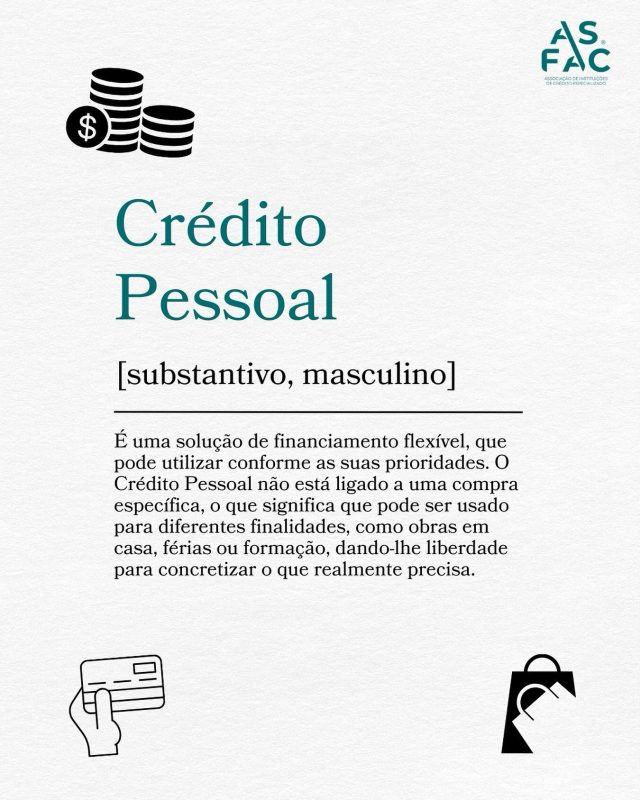

#CréditoPessoal 👉 Este é o conceito que trazemos esta semana na rubrica #ASFACDescomplica. 🙇♀️🙇

Tem que realizar uma despesa imprevista ou gostava de realizar um...

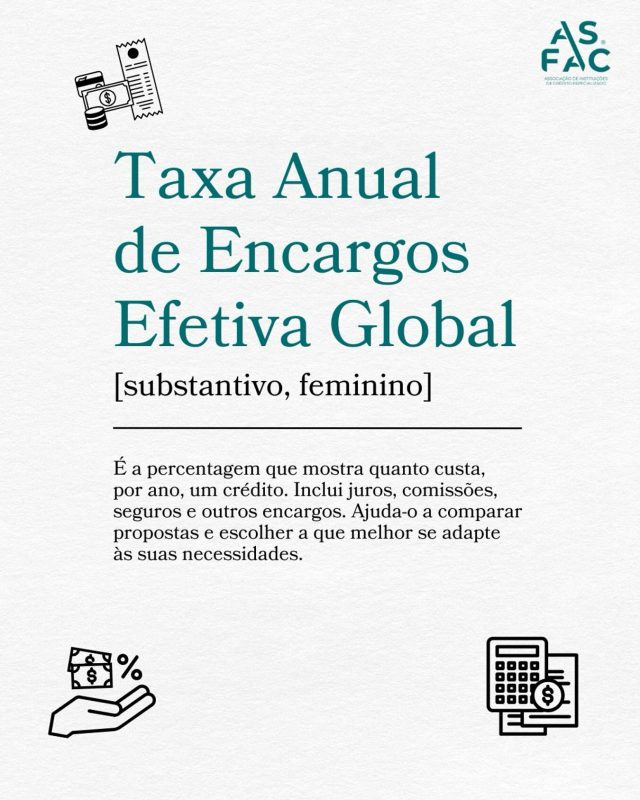

📘✨ Na rúbrica #ASFACDescomplica, trazemos-lhe mais um conceito fundamental para lidar melhor com as finanças do dia a dia.

Hoje explicamos a TAEG - Taxa...

🤝 ASFAC Descomplica 🤝

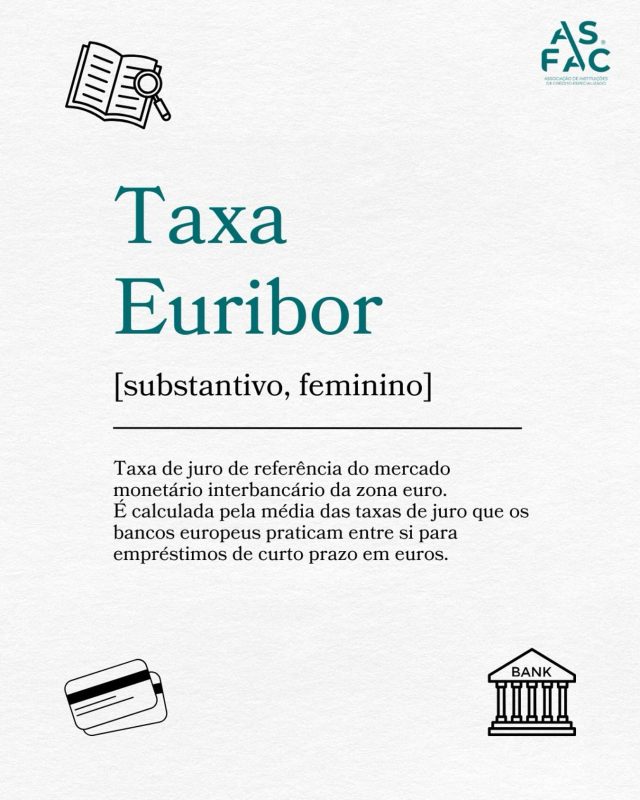

Quando falamos de #créditohabitação ou de outros #empréstimos, ouve-se muito falar da #Euribor. Mas o que significa ao certo? 🤔

Descomplicando,...

🤝 ASFAC Descomplica 🤝

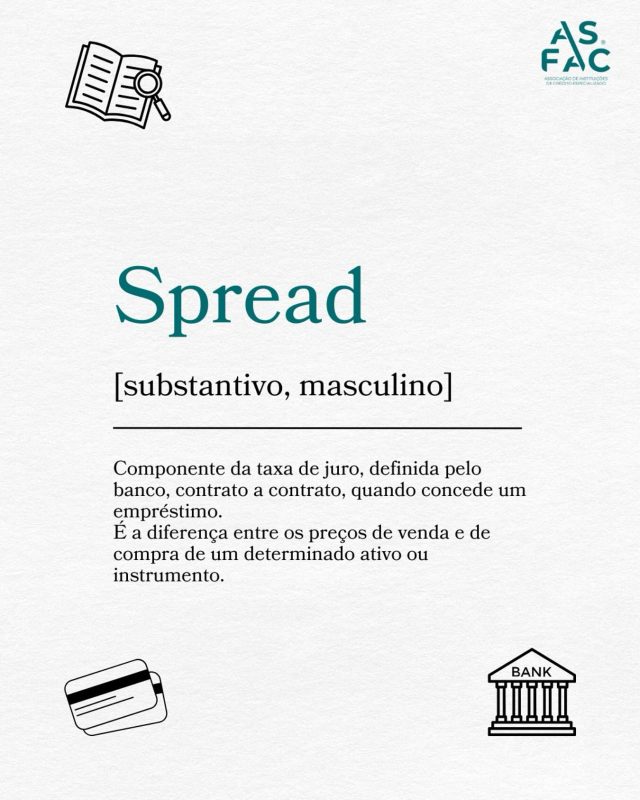

Já ouviu o termo spread quando pediu um #créditohabitação ou outros #empréstimos? E sabe do que se trata? 🤔

Descomplicando, o...

Os nossos associados